What’s the Plan? Where You Are in Life Matters.

A financial plan can help you to unlock different levels of your life. By mapping out your current lifestyle including your spending habits, debt control, and personal attitude toward finances and money management, we can help you to take control of your future and feel confident in your actions.

Think of it as a game of chess. Our goal is to learn about your dreams, anticipate your needs, and plan around possible scenarios of what will happen in the market and the world- and then we think three moves ahead so that you won’t have to make rash decisions in the future. We prepare for the worst with hopes of the best so that your plan reflects realistic scenarios of what could happen in your life.

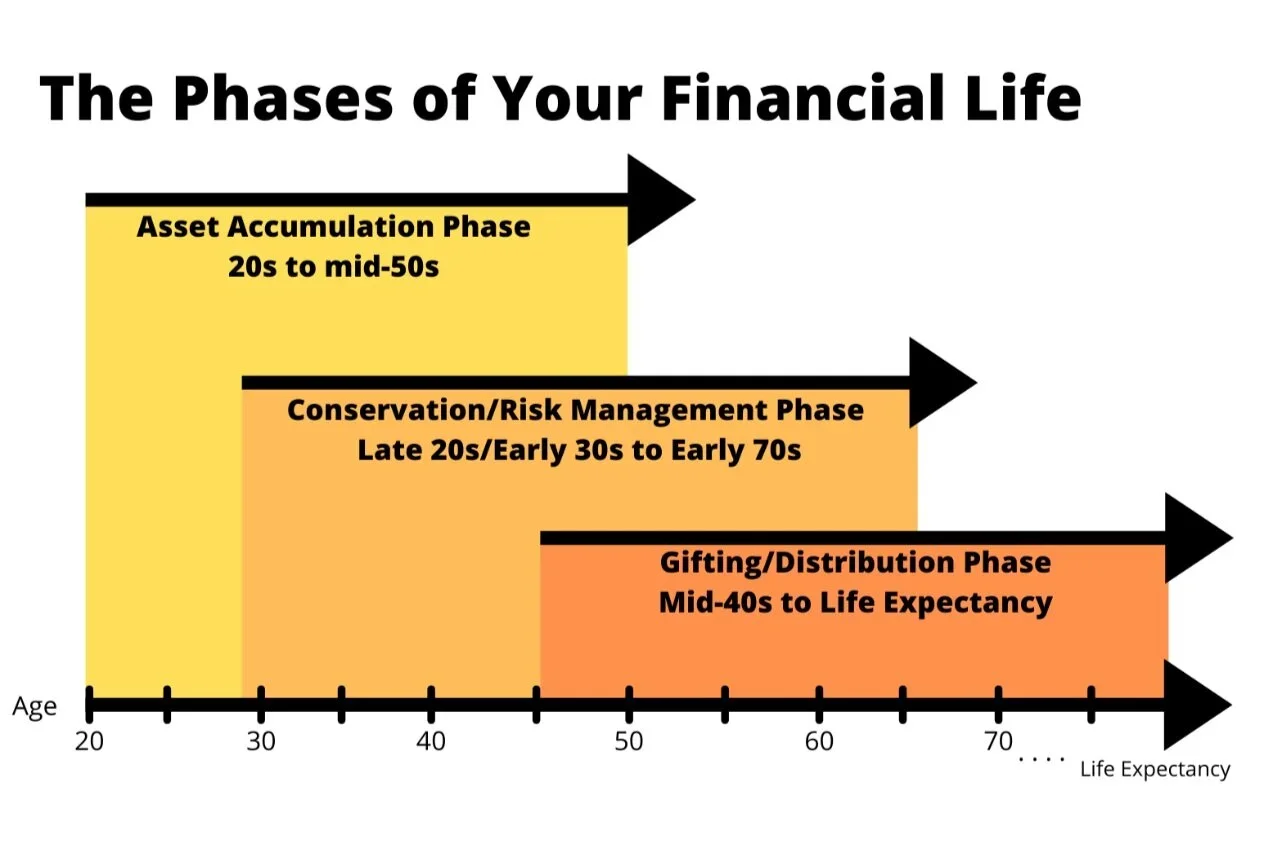

Where you’re at, in age and in life, matters to your plan. Per the chart above, we know that the phase of your life when you are accumulating wealth is between (but not limited to) ages 20-55. This is the phase where you want to invest as much as you can, and also save to fund emergency expenses. Following that, in your late 20s to early 70s, you’re in the Risk Management and Conservation stage where you’ll want to begin purchasing life insurance to cover your family’s needs in the event of a loss and to really dig into saving for retirement. The final phase of your Financial Life is the Gifting or Distribution phase from age 40 to the end of your life. This is when the kids have grown up and flown the nest and you are beginning to approach retirement, preparing to live the rest of your life comfortably and without financial worries. The gifting phase is truly unique. Some people are gifting to their children, some to charities, and some to themselves. Understanding the phase of your financial life that you’re in can help you to better prepare for the next steps.

Your plan using our planning software, is endlessly adjustable and allows us to prepare for the unexpected. It all starts with you making the conscious decision to take control of your finances and ends with us working together as a team to implement your plan and achieve your dreams.

To illustrate the usefulness and security that having a plan provides, we have drawn up a sample of circumstances that may resonate with you. If you have any questions or feel like a financial plan will benefit your family, please call our office and we will be happy to work with your family to make your lifestyle and financial dreams come true.

Daphne & Fred: Student Loan Payoff & College Savings for their daughter Velma

Fred and Daphne are both 30 years old and are in the asset accumulation stage of their financial life. They have multiple debts including a mortgage, credit cards, and student loans. Last year, they welcomed a new baby girl into the world, Velma. Realizing that they’re still paying off their own student loans made them begin to think that they wanted to help Velma avoid the same debts after graduating from college.

It took some homework on their part first to gather all of the information that we needed to build their plan together. From their statements, we took note that Fred had about $12k left in federal student loans, while Daphne had about $5k in private loans. Together, their gross income was $165,000 and they spend approximately $9,000 a month in totaling $108k per year. They felt that there was no end in sight to their debt and money management conundrum.

After inputting the data from their statements and conversations, we built the plan and came up with a few recommendations for Fred & Daphne to get out of debt and begin funding an education savings account for Velma.

Before they could begin to save for Velma’s education, we recommended that they pay off their current debts to make the most of their money, beginning with them paying off their credit card debt and student loans.

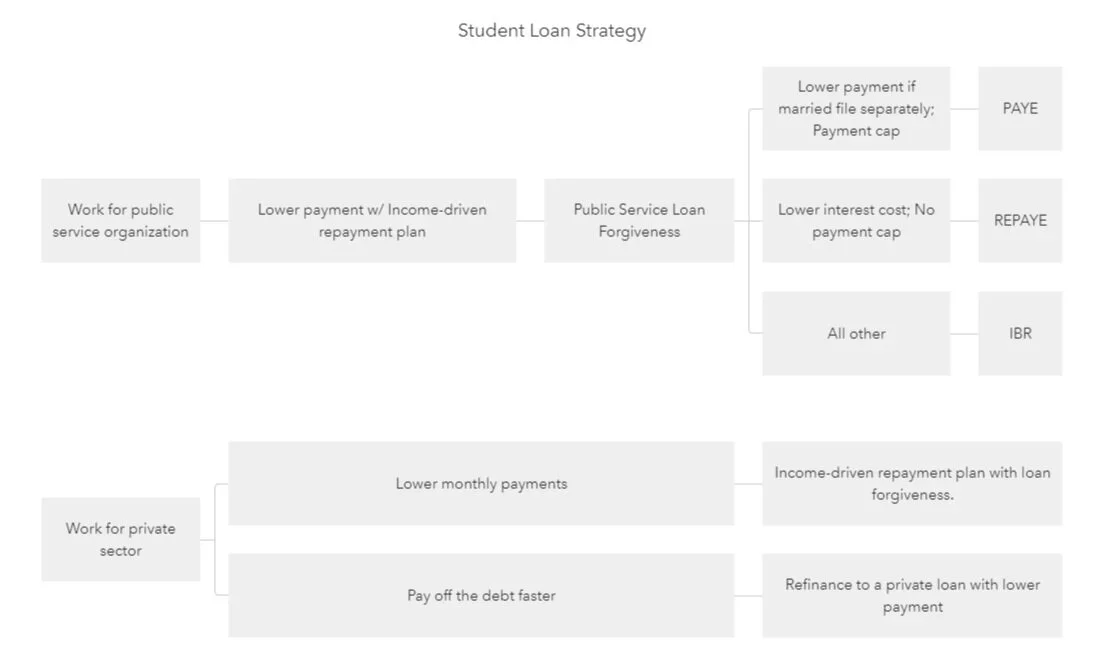

Below, you’ll see a graphic that represents the different student loan strategies available for Daphne and Fred. In Fred’s case, it would be recommended that he refinance his public student loan to a private lender to reduce his minimum monthly payment and to reduce the number of years until the debt is paid off.

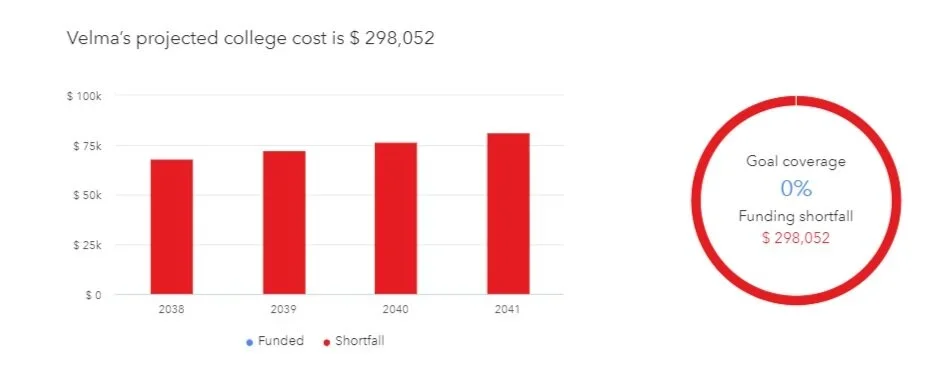

We used the national average cost for a public, four-year, in-state, on-campus college experience to estimate the overall costs for Velma’s education which was $26,820 per year, not including tuition inflation. Below, you will see the projected cost of college for Velma, and because the cost of tuition rises generally between 5-7% per year, it is essential to begin saving as soon as possible.

Following the crucial steps of paying off their debts by prioritizing those with the highest interest rates first and only paying the minimum on the others, Fred and Daphne realized that they could afford to help Velma to pay for school, but it would require discipline and guidance from their financial plan.

Now that their initial financial plan is complete, we work as a team, doing quarterly check-ins to maintain Fred and Daphne’s progress toward their goals.